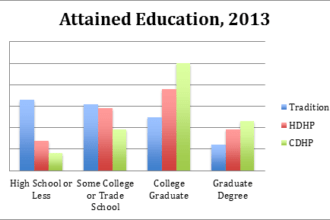

As most regular readers of this blog know, I’m self-employed. Fortunately, I don’t need to worry about health insurance, since I am covered through my husband’s job.

However, many are not so lucky, and must purchase a health plan on the open market. For a family of four, that can easily cost close to $20,000 annually. We all know people that would love to change jobs or perhaps start their own business, but remain tied to a position they dislike — even hate — because they need the benefits.

As most regular readers of this blog know, I’m self-employed. Fortunately, I don’t need to worry about health insurance, since I am covered through my husband’s job.

However, many are not so lucky, and must purchase a health plan on the open market. For a family of four, that can easily cost close to $20,000 annually. We all know people that would love to change jobs or perhaps start their own business, but remain tied to a position they dislike — even hate — because they need the benefits.

This scenario repeats itself millions of times across the country, according to a new report from the Robert Wood Johnson Foundation.

But in a few months, the benefits “job lock” won’t matter so much. Most of the remaining Affordable Care Act provisions fully kick in on January 1 — and the report says that greater self-employment and entrepreneurship will be one of the side benefits. They don’t see it as “unintended consequences,” but rather as an opportunity for people who might otherwise be hesitant to run their own show to do so, thanks to access to new health insurance marketplaces.

- Improved access and options to purchase health insurance through the marketplace. If you already have coverage, you can choose to remain with your current plan

- More preventive care – wellness screenings including mammograms, prostate exams, and pap smears must be covered by every plan, with no additional co-pay or deductibles. Mandatory well women screening benefits went into effect in August 2012.

- No denial of coverage for pre-existing conditions, being dropped from plans because of illness, and no more lifetime caps on benefits. Currently 129 million people under age 65 have at least one pre-existing health condition which could prevent them from obtaining new coverage if they leave their current plan. Starting next year, health insurers are generally prohibited from denying coverage because of a pre-existing condition or any other factor.

- Caps on premiums – insurers cannot establish separate “high risk” pools for people with existing illnesses, gender, occupation or claims history. Only age, tobacco use, and participation in wellness programs can be considered when setting rates. Renewal of coverage is guaranteed, regardless of health status.

Starting October 1, uninsured individuals and small business owners can begin signing up for insurance through state-based exchanges. Subsidies will be available for those meeting certain federal income criteria. You can determine your eligibility with this calculator.

If you’re a little (or a lot) confused, you’re not alone. Federal and state governments are training patient navigators to help guide consumers and small business owners through the enrollment process. They want as many people as possible to sign up early.

Do the math, former presidential advisor and vice provost for global initiatives at the University of Pennsylvania Ezekiel Emmanuel writes. The bigger the pool, the lower the premiums. He points to the “young invincibles,” the 20-something males — as key to making health exchanges work.

It’s not only the 20-somethings that are crucial to making exchanges work. It’s everyone. If you don’t have insurance, you will be required to obtain it or pay a penalty. If you are currently insured, you will have an option to switch plans down the road.

And if you’ve dreamed of starting your own business but haven’t because of insurance concerns, it may be the right time to resurrect those ideas.

![]()