Wound closure is a critical element of the overall wound management process. Indeed it is the most critical step in the sense that, if not accomplished promptly and effectively, can result in adverse outcomes ranging from chronic wound formation, infection and, unfortunately, death.

Wound closure is a critical element of the overall wound management process. Indeed it is the most critical step in the sense that, if not accomplished promptly and effectively, can result in adverse outcomes ranging from chronic wound formation, infection and, unfortunately, death.

Sealants and glues have become an entrenched, though not dominant, aspect of routine clinical practice in wound closure. These technologies have demonstrated efficacy that has warranted their use independent of other closure technologies, such as traditional sutures and staples, or as adjuncts to them, and some of these products also are being employed as general hemostatic agents to control bleeding in the surgical field. Manufacturers have also developed surgical sealants and glues that are designed for specific procedures – particularly those in which staples and sutures are difficult to employ or where additional reinforcement of the internal suture/staple line provides an important safety advantage.

Surgical sealants are made of synthetic or naturally occurring materials and are commonly used with staples or sutures to help completely seal internal and external incisions after surgery. In this capacity, they are particularly important for lung, spinal, and gastrointestinal operations, where leaks of air, cerebrospinal fluid, or blood through the anastomosis can cause numerous complications. Limiting these leaks results in reduced mortality rates, less post-operative pain, shorter hospital stays for patients, and decreased health care costs.

More Read

Although some form of suturing wounds has been used for thousands of years, sutures and staples can be troublesome. There are procedures in which sutures are too large or clumsy to place effectively, and locations in which it is difficult for the surgeon to suture. Moreover, sutures can lead to complications, such as intimal hyperplasia, in which cells respond to the trauma of the needle and thread by proliferating on the inside wall of the blood vessel, causing it to narrow at that point. This increases the risk of a blood clot forming and obstructing blood flow. In addition, sutures and staples may trigger an immune response, leading to inflamed tissue that also increases the risk of a blockage. Finally, as mentioned above, sutured and stapled internal incisions may leak, leading to dangerous post-surgical complications.

These are some of the reasons why surgical adhesives are becoming increasingly popular, both for use in conjunction with suture and staples and on a stand-alone basis. As a logical derivative, surgeons want a sealant product that is strong, easy-to-use and affordable, while being biocompatible and resorbable. In reality, it is difficult for manufacturers to meet all of these requirements, particularly with biologically active sealants, which tend to be pricey. Thus, for physicians, there is usually a trade-off to consider when deciding whether or not to employ these products.

It is useful to categorize surgical sealants, glues, and hemostats on the basis of their primary components and/or their intended use. The market for these products can be broken down (and has been done so in report #S192) by composition into products containing biologically active agents, products made from natural and synthetic (nonactive) components, and nonactive scaffolds, patches, sponges, putties, powders, and matrices used as surgical hemostats.

Global Market

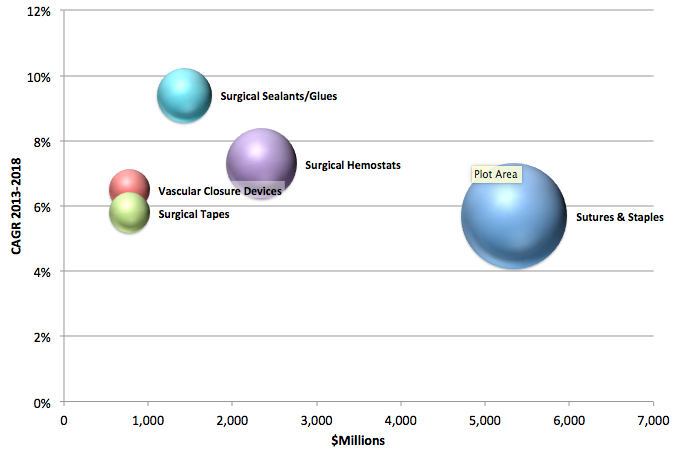

The global market for products in wound closure is comprised of large, well established, and relatively low growth segments like sutures/staples; the low volume, low growth segments like surgical tapes; and the smaller, higher growth segments like vascular closure, hemostats, and surgical sealants/glues:

Growth and Size of Major Wound Closure Market Segments

Sales ($millions) are 2014; Growth is CAGR 2013-2018.

Source: MedMarket Diligence, LLC; Report #S192 (published October 2014).

The MedMarket Diligence report #S192, “Worldwide Market for Surgical Sealants, Glues, and Wound Closure, 2013-2018: Established and Emerging Products, Technologies and Markets in the Americas, Europe, Asia/Pacific and Rest of World”, details the complete range of sealants & glues technologies used in traumatic, surgical and other wound closure, including tapes, sutures/staples, vascular closure, hemostats, fibrin sealants/glues and medical adhesives. The report details current clinical and technology developments, with data on products in development (detailing market status) and on the market; market size and forecast; competitor market shares; competitor profiles; and market opportunity. The Report provides full year actual data from 2013 and, for available companies, quarterly data from 2014. The report provides a worldwide forecast to 2018 of the markets for these technologies, with particular emphasis on the market impact of new technologies through the forecast period. The report provides specific forecasts and shares of the worldwide market by segment for Americas (detail for U.S., Rest of North America and Latin America), Europe (detail for United Kingdom, German, France, Italy, Spain, Rest of Europe), Asia/Pacific (detail for Japan, Korea, Rest of Asia/Pacific) and Rest of World.