One reason why entrepreneurs do what they do is that they want to become rich.

I don’t think that getting rich is the main motivation. The possibility of innovating in order to change the world may be an even stronger desire for most of them.

But you can almost guarantee there will be no entrepreneurship if you do two things: (a) eliminate all possibility of getting rich, and (b) make it impossible to change anything without the approval of an intractable bureaucracy.

One reason why entrepreneurs do what they do is that they want to become rich.

I don’t think that getting rich is the main motivation. The possibility of innovating in order to change the world may be an even stronger desire for most of them.

But you can almost guarantee there will be no entrepreneurship if you do two things: (a) eliminate all possibility of getting rich, and (b) make it impossible to change anything without the approval of an intractable bureaucracy.

That in a nutshell is my explanation for why our two most visibly dysfunctional social systems — health care and public education — remain so dysfunctional.

I meet entrepreneurs in health care almost every day. Their novel ideas are invariably focused on helping some entity — a hospital, insurer, employer, etc. — solve a problem. They are rarely focused on how to solve an overall social problem, however. Yet because our health care system is so dysfunctional, in solving the problem for a client, they may be making our social problems worse than they would have been.

Solving social problems in health care with innovative policy proposals is what I do. It is a lonely field. But it would be a lot less lonely if we allowed people to get rich doing it.

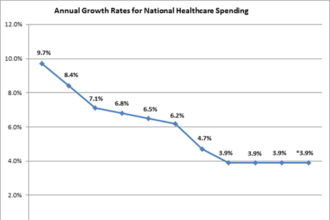

To take one example, it is often asserted that one-third of all health care spending is wasteful. Suppose Bill Gates was able to write a computer program that would find the waste and eliminate it. Society as a whole would save more than $800 billion. So how much should we be willing to pay Bill Gates? A tenth of the overall benefit he creates ($80 billion)? One-half the benefit ($400 billion)?

Perhaps you’re thinking that we shouldn’t pay Bill Gates anything. Maybe you think he should give us the program for free, as an altruistic gesture. Or, maybe you think the most he should get back is a 1% or 2% return — something close to the return paid by government bonds. If this is your viewpoint, welcome to the world of health policy. You will find all kinds of people who think just like you do.

He’s your guy when stocks are high

but beware when they start to descend

In general, there is no limit to how much people can make in health care by successfully exploiting reimbursement formulas. But the federal government is in the process of limiting what insurance companies can earn, effectively reducing them to the role of public utilities.

Two recent items in the news help illustrate why this approach is so wrong. In one, The New York Times reports:

The brothers, Philip and Joel, earned close to $1 million a year each as the two top executives running a Medicaid-financed nonprofit organization serving the developmentally disabled.

They each had luxury cars paid for with public money. And when their children went to college, they could pass on the tuition bills to their nonprofit group.

Philip H. Levy went as far as charging the organization $50,400 for his daughter’s living expenses one year when she attended graduate school at New York University. That money paid not for a dorm room, but rather it helped her buy a co-op apartment in Greenwich Village.

In the other story, The New York Times reports that BlueShield of California will voluntarily limit its profit to no more than 2% of revenues — no doubt anticipating that government regulators were going to force that result anyway.

Think about those two examples. Almost everybody in health care agrees that many of our biggest problems stem from the way we pay for care. And who is paying? Insurance companies. So another way of stating the social problem is: we need to find newer and better types of third-party payment.

Yet we are living in a world in which entrepreneurs are encouraged to make unlimited amounts of money exploiting reimbursement formulas, but are not allowed to make any extra money making the formulas better and more effective.

Let’s suppose that an insurance company contracts with Bill Gates for the hypothetical software described above. By using it, the insurer will cut its spending one-third and add that amount to the bottom line. But under ObamaCare, the software will never be invented, never be purchased and never be used. Why? Because under the new health law it will be impossible for an insurer to cash in on that innovation.

An insurer’s medical loss ratio (MLR) is the percent of its premiums spent on medical care. The remainder includes administrative costs and profit. As reported previously, the new law establishes a minimum MLR of 80% for most insurers and 85% for large insurers like BlueCross.

This is intended, among other things, to make sure that insurance companies do not have above-normal profits. As an additional hammer, the Obama administration is encouraging state governments to aggressively regulate insurance premiums, and if they are not aggressive enough, the federal government is threatening to step in and do the job from Washington.

Absent ObamaCare, BlueCross could use Bill Gates’ hypothetical software to achieve a MLR of 55%. That would be good for numerous reasons: the elimination of wasteful spending would improve the quality of care for patients, reduce the chance of medical errors, free up resources for use by other patients and encourage every other insurer to find ways of achieving the same outcome.

But with the new health reform law, BlueCross would have to rebate its 33% profit to enrollees in the form of lower premiums. Thus, neither BlueCross nor any other insurer will be able to profit from cost-reducing discoveries like this one. Nor will any insurer even try. Instead, insurance companies will function like utilities, taking no real risks and making no radical changes in their current business model.

ObamaCare has ensured that our health care problems will not be solved by stifling innovation in the one sector of the market that most needs vigorous entrepreneurial activity.